Hospital Cover vs Day-to-Day Cover NZ: A Comprehensive Guide

Estimated Reading Time: 7 minutes

Key Takeaways

- Hospital Cover addresses in-patient treatments and surgeries, while Day-to-Day Cover reimburses routine healthcare expenses.

- Private medical cover offers faster specialist access, provider choice, and reduced wait times compared to the public system.

- Pre-existing conditions can lead to exclusions, loading fees, or extended waiting periods—full disclosure is essential.

- Waiting periods vary: 3–12 months for hospital services and 2–6 months for certain day-to-day treatments.

- No government rebate exists in NZ; policy value and premium levels should be checked closely.

Table of Contents

Understanding Private Medical Cover in NZ

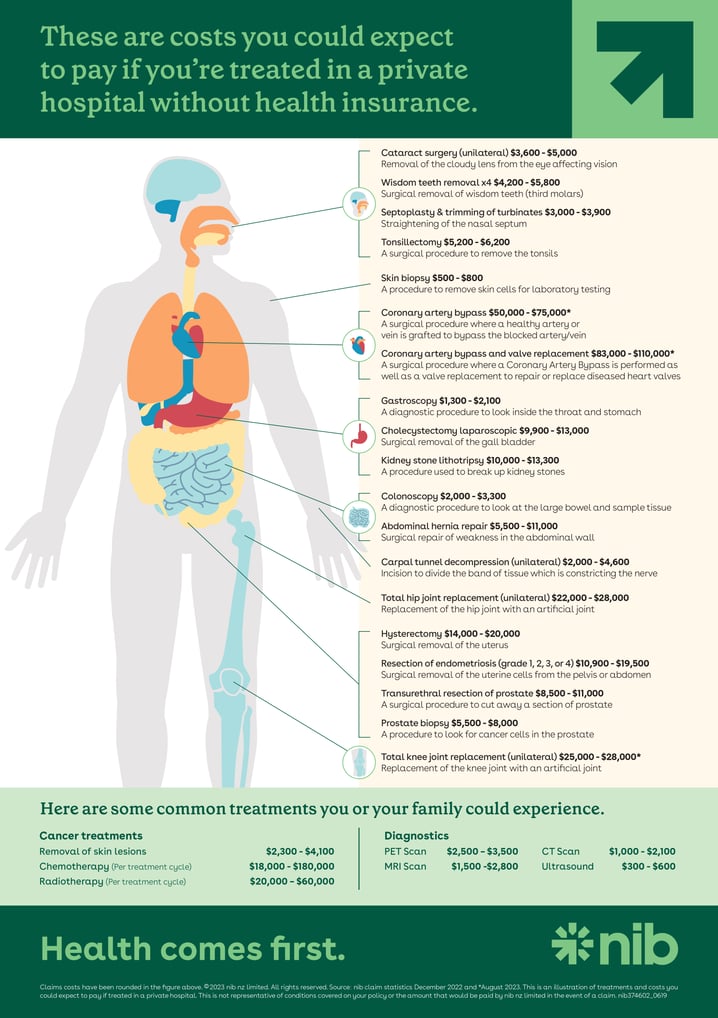

Private medical cover in New Zealand supplements the public health system by covering costs not fully subsidised by public hospitals. The two main components are Hospital (Surgical) Cover and Day-to-Day (Everyday) Cover. These policies deliver quicker specialist access, more choice of providers, and reduced public wait times. For a full comparison of plans and cost breakdowns, see our private health insurance comparison.

Benefits of Private Medical Cover

- Faster Access to Specialists: Avoid public hospital waitlists.

- Choice of Provider: Decide who treats you and where you receive care.

- Reduced Wait Times: Access procedures and consultations without lengthy delays.

Hospital Cover vs Day-to-Day Cover

Hospital Cover

- Main Use: In-patient treatments, surgeries, specialist fees, and private hospital accommodation.

- Benefits: Covers large, unexpected medical costs and bypasses public waitlists (Southern Cross).

- Exclusions: Routine check-ups and everyday services are typically not covered.

- Premium Cost: Generally higher due to the potential size of claims.

- Claims Process: Providers often bill the insurer directly.

Day-to-Day Cover

- Main Use: GP and nurse visits, dental and optical services, prescriptions, physiotherapy, vaccinations, and basic tests.

- Benefits: Reduces regular out-of-pocket expenses for routine care (Nib; Accuro).

- Exclusions: Does not cover major surgeries or inpatient treatments.

- Premium Cost: Lower premiums with smaller claim limits.

- Claims Process: You pay upfront and claim reimbursement from the insurer.

Use Case Scenarios

- Young, Healthy Adult: Prefers Day-to-Day Cover for routine check-ups and prescriptions.

- Family: Combines both covers to protect against hospital stays and manage regular healthcare costs.

- Older Adult: Prioritises Hospital Cover to safeguard against major, costly medical events (LifeCovered; Accuro).

Pre-Existing Conditions Health Insurance NZ

A pre-existing condition is any health issue with signs, symptoms, or treatment before your policy start date. New Zealand insurers typically manage these through:

- Exclusions: Certain conditions may never be covered.

- Loading Fees: You may pay higher premiums.

- Extended Waiting Periods: Delays before you can claim for related services.

Full disclosure of your medical history is legally and financially essential to avoid denied claims.

Tips for Accurate Declaration

- List all past and current medical treatments.

- Obtain a comprehensive health check before applying.

- Provide detailed information in your application forms.

Health Insurance Waiting Periods NZ

Waiting periods are the time between policy inception and when you can claim certain services. Hospital cover waiting periods typically range from 3–12 months, especially for pre-existing conditions. Day-to-day cover may allow immediate GP visits but impose 2–6 months for dental and optical services (Abacus Group; Accuro).

Strategies to Minimise Waiting Periods

- Apply well before anticipated healthcare needs.

- Maintain continuous coverage when switching insurers.

- Understand each insurer’s rules on policy breaks.

Health Insurance Rebates NZ

Unlike Australia, New Zealand has no government rebate scheme for private health insurance premiums (Abacus Group). Review your policy’s value and premium levels carefully, as no financial safety net exists. Should rebates be introduced in the future, they will likely depend on income tiers and be handled via insurer portals.

Building the Right Policy for You

Follow these steps to tailor a private health insurance policy:

- Assess Health Needs: Review personal/family health history, treatments, and risk factors.

- Decide on Cover Mix: Choose Hospital, Day-to-Day, or combined cover based on your requirements.

- Compare Policies: Evaluate claim limits, exclusions, gap payments, loading fees, and waiting periods via our comparison.

- Key Questions for Insurers:

- What are your excess and gap payment policies?

- How do you handle pre-existing conditions?

- What are the exact waiting periods?

- Review Rebate Options: Stay informed on potential rebates and ensure policy flexibility for life-stage changes.

Conclusion

Choosing between Hospital Cover and Day-to-Day Cover in New Zealand hinges on your personal health needs and budget. Hospital Cover protects against major, unforeseen medical costs, while Day-to-Day Cover reduces routine out-of-pocket expenses. Understanding pre-existing condition rules, waiting periods, and the absence of rebates empowers an informed decision. Audit your current policy or connect with a licensed adviser for a tailored health insurance solution—see our full private health insurance comparison for more details.

FAQ

What’s the main difference between Hospital Cover and Day-to-Day Cover?

Hospital Cover covers inpatient and surgical procedures, while Day-to-Day Cover reimburses everyday healthcare visits and services.

Can I combine Hospital and Day-to-Day Cover?

Yes. Many Kiwis choose combined cover to ensure protection for both major medical events and routine healthcare needs.

How do waiting periods affect my coverage?

Waiting periods delay when you can claim benefits. Hospital cover waits are 3–12 months; day-to-day waits vary by service (2–6 months).

Will pre-existing conditions be covered?

Insurers may apply exclusions, loading fees, or extended waits for pre-existing conditions. Full medical disclosure is essential.

Are there any government rebates for health insurance in NZ?

Currently, New Zealand has no government rebate for private health insurance premiums.