Life Insurance NZ Comparison: Cheapest & Best Policies for 2025 (+ How to Get Instant Online Quotes)

Estimated reading time: 10 minutes

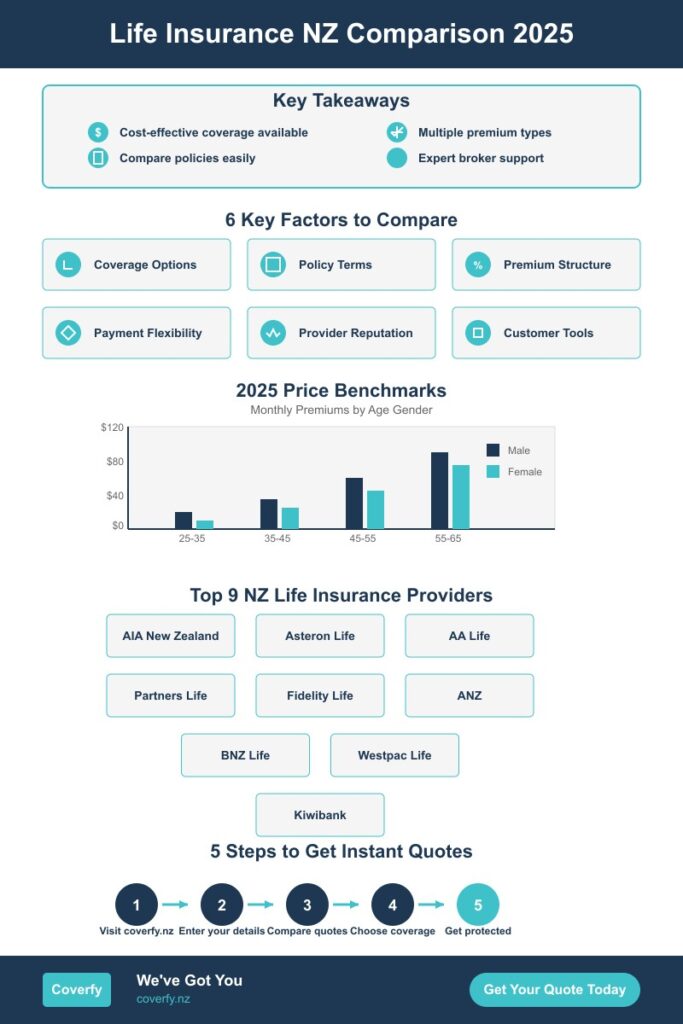

Key Takeaways

- A thorough life insurance NZ comparison helps you secure cost-effective and reliable coverage.

- Key factors include coverage options, policy terms, premium structures, and payment flexibility.

- Online quotes provide a fast and impartial way to compare multiple offerings.

- Using a life insurance NZ broker can offer tailored advice and simplify the process.

Table of Contents

- Introduction

- Quick Primer: How Life Insurance Works in NZ

- Why Compare Life Insurance in NZ?

- 6 Key Factors to Assess

- Cheapest Life Insurance NZ: 2025 Price Benchmarks & Savings Tips

- Best Life Insurance NZ 2025: Top 9 Providers

- Step-by-Step: How to Get Instant Online Quotes

- Do You Need Life Insurance NZ Brokers?

- Side-by-Side Comparison Table

- Decision Checklist & Next Steps

- Conclusion

- FAQ

Introduction

A thorough life insurance NZ comparison is the quickest route to affordable, reliable cover. For many New Zealanders, understanding the array of options when it comes to life insurance is crucial before making a commitment. This article delves into the nuances of life insurance in NZ, examining price benchmarks for 2025, identifying market‐leading providers, exploring how to secure online life insurance quotes in NZ, and discussing the role of life insurance NZ brokers. For more details on securing those quotes, check out our Instant Quotes Guide. This comprehensive guide serves as your gateway to making informed choices in the life insurance landscape.

Quick Primer: How Life Insurance Works in NZ

Life insurance policies in New Zealand generally fall under term life insurance, which provides a lump sum payment on the occurrence of death or a terminal illness diagnosis during the term of the policy. Options such as trauma cover, total and permanent disability (TPD) cover, and various add‐on riders like child cover or mortgage repayment protection are also available. The industry is regulated by both the Financial Markets Authority (FMA) and the Reserve Bank of New Zealand, ensuring insurers maintain solid financial footing and uphold fair conduct.

If you’re new to the different coverage types, check out our post on Insurance Policy Types in NZ for a more detailed breakdown.

Why Compare Life Insurance in NZ?

Comparing life insurance policies allows you to secure comprehensive benefits for your budget, avoid hidden fees and exclusions, access discounts and promotions, and ensure reliable customer service. By comparing plans from different NZ providers, you can avoid overpaying while ensuring your family remains protected.

For further insights, visit MoneyHub and Quashed.

6 Key Factors to Assess in a Life Insurance NZ Comparison

Coverage Options & Benefits

Understand what each policy covers—such as death cover, terminal illness, trauma, TPD—and the optional riders available. These features determine how well you and your family are protected financially.

Learn more at Life Covered NZ.

Policy Terms & Conditions

Policies vary in their terms, particularly concerning exclusions like pre‐existing conditions and suicide, as well as clauses such as waiting periods and renewal options.

Premium Structure

Explore the differences between stepped and level premiums. Stepped premiums may initially be cheaper but increase over time, whereas level premiums remain consistent, offering predictable costs.

For an in-depth look, see Premium Structures Explained and MoneyHub.

Payment Flexibility & Discounts

Consider insurers that offer flexible payment options (annual vs. monthly) and discounts for non‐smokers or those with multiple policies.

Provider Reputation & Claims History

Review the insurer’s financial health and claims payout history to gauge reliability and performance.

More details can be found at Life Covered NZ.

Customer Service & Digital Tools

Evaluate the availability of digital tools for policy management and customer support, ensuring you receive prompt assistance when needed.

Cheapest Life Insurance NZ: 2025 Price Benchmarks & Savings Tips

In 2025, women aged 20-30 may find premiums as low as $20–$21 per month, whereas men in the same age range might face rates from $23–$33. Premiums tend to rise with age, emphasizing the need to secure a beneficial rate early.

Here are some tips to potentially lower your premiums:

- Opt for Stepped Premiums: Start with stepped premiums when younger, and consider switching to level premiums later on to balance cost and coverage.

- Maintain a Healthy Lifestyle: Staying fit can reduce your risk profile and lower premiums.

- Bundle Policies: Combining life insurance with other policies may result in discounts on overall costs.

- Annual Payments: Paying annually can often secure further discounts.

Providers such as AIA, Partners Life, and Pinnacle Life are frequently mentioned in discussions around “cheapest life insurance NZ.”

Visit MoneyHub and Quashed for more information.

Best Life Insurance NZ 2025: Top 9 Providers & Why They Rank

2025’s Top Providers

- AIA – Known for its global capital strength and innovative Vitality wellness rewards.

- Asteron Life – Offers robust trauma and TPD cover options.

- AA Life – A trusted brand with straightforward policies.

- Fidelity Life – Renowned for local expertise and high-quality customer service.

- Partners Life – Praised for flexible underwriting processes and extensive rider options.

- Pinnacle Life – Recognised for competitive pricing and fully online services.

- Southern Cross Life – Noted for its combined health and life insurance solutions.

- Chubb Life – Focuses on premium clients with complex insurance needs.

- Westpac Life – Integrates banking solutions with insurance for added convenience.

The NZ life insurance sector is expected to grow significantly by 2025, driven by economic recovery and increased market awareness.

For more details, check out Life Covered NZ and Insurance Asia.

Step-by-Step: How to Get Instant Online Life Insurance Quotes NZ

- Choose a Comparison Site: Start with platforms such as MoneyHub, LifeDirect, or Quashed for comprehensive comparisons.

- Input Personal Details: Provide your date of birth, gender, smoking status, and desired coverage amount.

- Adjust Options: Experiment with different riders and premium structures to see how these affect your quotes.

- Review and Compare: Assess conditions and exclusions outlined in each quote.

- Narrow Down Choices: Select a few providers for further investigation or discussion with a broker.

This method is free and unbiased, allowing you to compare offerings side-by-side. For further guidance, check out our post Online Quotes Made Simple.

Refer to resources from MoneyHub, Quashed, and Life Covered NZ.

Do You Need Life Insurance NZ Brokers? Pros, Cons & How to Choose

Benefits of Using a Broker

- Tailored Advice: Brokers assess your personal and financial situation to offer customised recommendations.

- Ease of Use: They manage paperwork and clarify policy fine print, streamlining the process.

- Negotiation Leverage: Experienced brokers negotiate better policy terms on your behalf.

- Support for Claims: In case of a claim, a broker’s advocacy can be invaluable.

Choosing the Right Broker

Ensure the broker is registered with the FMA and is a member of a professional body such as Financial Advice NZ. Review client testimonials and be clear about fee structures and any commission-related conflicts. For more guidance, read our guide on Finding the Right Insurance Broker.

Also, refer to resources from MoneyHub and Life Covered NZ for additional insights.

Side-by-Side Comparison Table: Major NZ Providers

| Provider | Strengths | Potential Drawbacks | Entry Premium* | Key Riders |

|---|---|---|---|---|

| AIA | Global capital, Vitality rewards | Complex options | $XX | Yes |

| Partners Life | Flexible cover | Higher premiums for 50+ | $XX | Yes |

| Pinnacle Life | Budget online | Fewer riders | $XX | No |

| AA Life | Brand trust | Limited cover choices | $XX | Minimal |

| Fidelity Life | Strong service | Higher cost vs online-only | $XX | Optional |

*Premiums are indicative as of March 2025. Please check directly with providers for current rates.

Decision Checklist & Next Steps

- Ensure the cover amount matches your needs.

- Review all policy exclusions thoroughly.

- Compare premium structures (stepped vs. level) to see what suits you best.

- Read the product disclosure statement before finalising your choice.

- Consult with a broker if you have any uncertainties.

- Secure your quotes promptly as rates can change monthly.

Compare Quotes Now to take the next step in securing the right coverage for your needs.

Conclusion

Conducting a meticulous life insurance NZ comparison not only helps you lock in cost-effective premiums but also ensures you receive robust protection in 2025. Whether you opt for instant online quotes or consult with a trusted broker, taking informed action today can secure financial peace of mind for you and your family.

Please visit the MoneyHub, Quashed, and LifeDirect websites for further guidance and to access tailored life insurance quotes. Their resources can simplify your decision-making process, ensuring the best coverage for your circumstances.

FAQ

What are the benefits of comparing life insurance policies?

Comparing policies allows you to identify the best value coverage tailored to your individual needs, helping you avoid hidden fees and unnecessary costs.

Can I get life insurance online?

Yes, many providers now offer instant online quotes and digital tools, making it easy to compare options and manage your policy conveniently.